Tax season can leave you asking lots of questions, especially about what you can and can’t deduct. If you spend a lot on dry cleaning for work, it might seem logical to save money by deducting those costs. After all, laundry bills can pile up fast... Read More

Navigating tax deductions can get tricky, especially when it comes to medical expenses like eyeglasses. Every year, many Americans wonder if the cost of their reading or prescription eyeglasses can help reduce their overall tax burden. While the I... Read More

Tax season can be tricky, especially when you’re figuring out which expenses can lower your tax bill. If you’ve supported political candidates, parties, or campaigns, you might wonder if those contributions can help you during tax time. With all t... Read More

When it comes to filing taxes, the process can feel overwhelming, especially when considering which expenses tax deductible qualify. If you or your child needed braces, you may be wondering if the cost can help reduce your taxable income. Braces a... Read More

You've been going to therapy for a while now, and it's been helping you immensely. The regular sessions with your therapist have improved your mental health, helped you manage stress and anxiety, and provided you with the tools to cope with challe... Read More

Are you wondering whether assisted living expenses are tax deductible? If you are a senior or have family members in assisted living, this may be an important question to consider. Can you actually deduct the costs of assisted living on your tax r... Read More

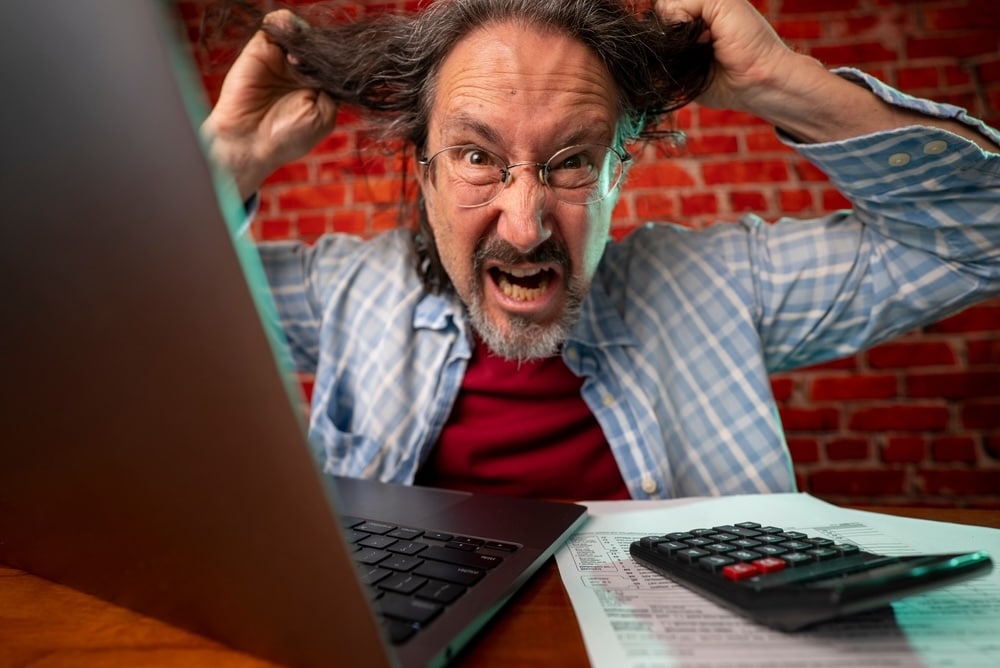

You're sitting at your kitchen table, surrounded by a mountain of receipts and financial documents. The clock is ticking down to tax day, and you're wondering how much you'll owe. Are there any parts of this process that could save you some money?... Read More

You're a skilled lawyer, accountant, or consultant, and you've come across a local nonprofit organization that desperately needs your expertise. However, they can't afford your professional fees. You decide to offer your services pro bono, driven ... Read More

Half of the year is gone and you suddenly remember that you barely used the expensive gym membership you impulsively bought in January. You start to wonder if there's a way to make the most out of your momentary fitness motivation, and it dawns on... Read More

Are you spending too much on adult diapers? Perhaps you have a dependent who requires the use of adult diapers due to an illness/injury, or maybe you yourself are in need of them. Regardless of the reason, one question that may have crossed your m... Read More